Market Recap

US Markets:

Stocks fell on Friday due to concerns of rising new coronavirus cases, and questions around stimulus and emergency funding. With new shutdown measures implemented, the vaccine-related euphoria has been subdued, and doubt has been cast on a swift economic recovery.

The Dow Jones dropped 219 points, or 0.8%, the S&P 500 dipped 0.7%, and the Nasdaq closed down 0.4%, erasing earlier gains. The small-cap Russell 2000 index once again outperformed the larger indices, rising by .07%.

COVID cases in the U.S. continue surging to record highs. The seven-day average of daily new Covid-19 infections now stands at 165,029- 24% higher than a week ago. As the CDC advised Americans against traveling for Thanksgiving, California Gov. Gavin Newsom also issued a “limited Stay at Home Order” requiring nonessential work and gatherings to cease between 10 p.m. and 5 a.m.

JPMorgan economists today were also the first on Wall Street to forecast negative GDP growth for the start of next year, downgrading their first-quarter GDP outlook to a contraction of 1%.

Also weighing on sentiment Friday was a disagreement between the Treasury Department and the Federal Reserve over the continuation of several emergency funding programs. While Treasury Secretary Steven Mnuchin is seeking to end many of these programs, the Fed is pushing back, saying that these programs serve an important role in supporting the economy. Markets do not like uncertainty- especially with economic stimulus- and they reacted accordingly today.

On the bullish side of things, there was more good vaccine news as Pfizer and BioNTech said that they will apply for an emergency use authorization for their vaccine from the FDA. If all goes as planned, they could be ready to ship the vaccine within hours.

Today’s losses led the Dow and S&P 500 to their first weekly declines in three weeks, with the Dow falling 0.7% this week and the S&P 500 losing 0.8% this week. Although there is a light at the end of the tunnel, until the pandemic goes away for good, investors will continue wrestling with long-term optimism and short-term reality.

Cryptocurrency:

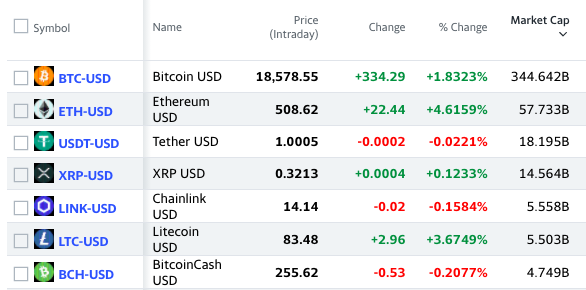

Bitcoin continues to be on a record run, and finally broke past the $18,500 resistance level. Although Bitcoin has seen near-term resistance as of late at the $18,500 level, breaking through this key level is a major milestone on the path to $20,000. Bitcoin’s value has more than doubled this year, and has not traded this high since early-January 2018. In fact, Bitcoin has rallied 75% in less than three months, and gained almost 400% since March. With coronavirus stimulus measures, validation from public companies such as Square and Paypal, and interest from major investors, the case for Bitcoin has arguably never been this bullish before. Many believe Bitcoin could reach $20,000 before year’s end as many expect the cryptocurrency to consolidate. Billionaire investor Mike Novogratz also predicted that the price of bitcoin would hit $65,000 eventually. Ethereum also popped over 4.6% today, and Litecoin continued its strong run as well, gaining another 3.67%, and breaking a key resistance level of $80.

Overall Market:

European markets closed higher on Friday- good for their 3rd weekly gain in a row. Frankfurt’s DAX 30 rose 0.4% to end at 13,137, while all other major European indices gained between 0.3% and 0.8%. However, European Union leaders were still at an impasse with regards to unlocking a €1.8 trillion budget and pandemic recovery package. Talks between the EU and UK over Brexit were also suspended after one of the negotiators tested positive for the coronavirus. Eurozone consumer morale also weakened in November, and fell 2.1 points from the previous month to -17.6 in November 2020-the lowest the level has been since May. Meanwhile, Canada’s TSX rose by .7% led by gains in materials stocks, and a greater rise in Canadian retail sales than expected.

Despite the fears of COVID spikes permeating through the markets, gold surprisingly lagged yet again. Usually seen as a safe haven asset, gold suffered its second consecutive week of losses, and dropped 0.8% this week to settle at $1,873 per ounce. Copper also hit a 6-1/2-year high and crossed $3.3 per pound for the first time since February 2014, supported by COVID vaccine optimism, growing demand from top consumer China, and a decline in Chile’s production. Lumber prices also hit its highest level since September 15th, and crude oil booked its third consecutive week of gains, rising 5% for the week and settling at $42.2 per barrel.

WHATS UP

Boeing and Salesforce were the worst-performing stocks in the Dow, falling 2.9% and 2.5%, respectively.

Financials and industrials also were the leading laggards on the S&P 500, and dropped 0.9% and 1.1%, respectively.

Cyclical recovery stocks were also battered today, with cruise lines Norwegian and Carnival dropping 4.9% and 4.5% respectively, and Las Vegas Sands also falling 4.5%.

Zoom led the markets amidst an increase of investors piling back into stay-at-home stocks, and popped over 6%.

Source: CNBC, TradingEconomics, Stockcharts, Yahoo! Finance