Market Recap

US Markets:

U.S. stocks recovered losses from yesterday, and jumped to kick off December. November’s rally continued on to start the final month of 2020- a year which has been quite trying and difficult.

The Dow Jones climbed 185.28 points, or 0.6%, to 29,823.92, and jumped more than 400 points at its session high to a new intraday record. The S&P 500 also rose 1.1%, or 40.82 points, to a record closing high of 3,662.45. The Nasdaq also closed at a record high and gained 1.3%.

Sentiment was boosted after lawmakers revealed a $908 billion stimulus plan that included over $200 billion in Paycheck Protection Program small business loans. In addition to stocks, the 10-year Treasury yield also rose above 0.9%.

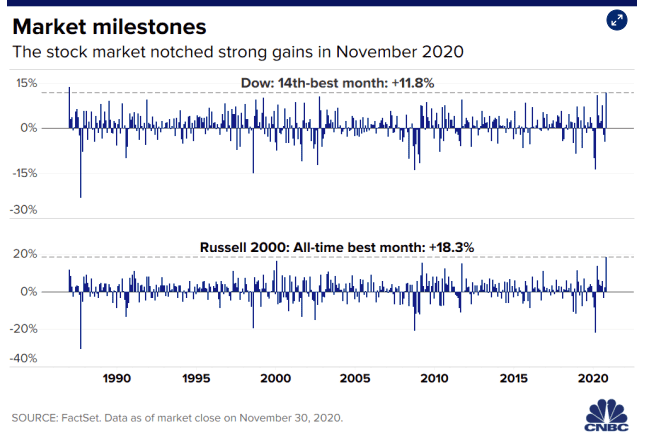

The Dow rallied 11.8% in November, posting its best one-month performance since January 1987. The S&P 500 and Nasdaq Composite also rose 10.8% and 11.8%, respectively, for their strongest monthly gains since April. After November’s gain and Tuesday’s rally, the S&P 500 is now up 13.8% for 2020.

Value stocks and small-caps led last month’s rally. These are stocks largely dependent on an economic comeback. The iShares Russell 1000 Value ETF (IWD) rallied 13.4% for the month, and outperformed its growth counterpart, the iShares Russell 1000 Growth ETF (IWF), by more than 3%. The small-cap Russell 2000 also had its best month ever and rose more than 18%.

Political stability and strong coronavirus vaccine data spurred on November’s rally. In the latest vaccine news, Pfizer and BioNTech applied to the European Medicines Agency for conditional marketing authorization of their coronavirus vaccine. This could potentially put the vaccine in full use in Europe before the end of 2020.

However, not all is well. Both Federal Reserve Chairman Jerome Powell and Treasury Secretary Steven Mnuchin spoke before Congress on Tuesday, with Powell stating that the economic outlook for the U.S. was “extraordinarily uncertain,” and that the surge in COVID-19 cases “could prove challenging for the next few months.” Powell further said that a full economic recovery is unlikely until people feel safe and confident.

According to data compiled by Johns Hopkins University, more than 13 million COVID-19 cases have been confirmed in the U.S. along with over 266,000 deaths. Shutdown and emergency measures continue to be reimposed, including New York Gov. Andrew Cuomo’s announcement today that the state was reimplementing emergency hospital measures.

ISM data also showed that US factory growth slowed in November. According to the ISM Manufacturing report, PMI for the US fell to 57.5 in November of 2020 from a two year high of 59.3 reached in October. Although figures came in slightly lower than market forecasts of 58, they still pointed to expansion in the overall economy for the seventh month in a row.

Cryptocurrency:

Crypto’s did not move much today, however some pulled back. After surging last month, XRP pulled back by around 8.17% today. BitcoinCash also dropped 6.13% today after surging by over 7.63% yesterday. After hitting an all-time intraday high yesterday, and trading as high as $19,864, Bitcoin somewhat pulled back today and traded around the $19,000 level. Although Bitcoin still has not hit $20,000 yet, it has now shattered its previous record of $19,666 from back in December 2017. Bitcoin’s value is now up over 150% since the beginning of the year, and has been propelled by economic stimulus, validation from public companies such as Paypal, and interest from major investors. Although some believe a Bitcoin correction is inevitable, others believe that it could exceed $20,000 as a hedge against inflation before the end of the year.

Overall Market:

European indices followed strong November gains with more gains to kick off December. The German DAX 30 added 91 points or 0.7% to hit a 9.5 month high. Other European indices were up between 0.3% and 2%, largely buoyed by prospects that a Covid-19 vaccine could soon hit the market. Additionally, the China Caixin/Markit Manufacturing PMI for November came in at 54.9, the highest reading in a decade. These results further show how the Chinese economy has robustly rebounded from the hit of the pandemic. Canada’s TSX also rallied to close above 17,300 due to a rally in materials and financials, and upbeat GDP data. Recent data showed that the Canadian economy expanded at the fastest rate ever in the third quarter. Mexico business sentiment also improved to an 8-month high.

WTI crude futures fell for a second day in a row, and fell more than 1% to around $44.75 a barrel. Delays until Thursday in OPEC+ talks regarding crude production sent the commodity lower, as producers were still in disagreement on how much oil they should produce. Unusual tensions between Saudi Arabia and UAE also weighed. Meanwhile, Copper futures climbed to a 7-1/2-year high to above $3.48 per pound, and extended a 12.4% rally in November. Natural gas also rallied to near $3.

WHATS UP

Electric-car maker Tesla popped 2.7% after the S&P said that they will be added to the S&P 500 on Dec. 21 in a single step- despite its large size.

Apple also rose 3% along with Intel to lead the Dow higher. Communications and financials led the S&P 500, rising at least 1.9% each.

Zoom Video was the laggard of the day, however, and fell 15.3% despite reporting better-than-expected earnings for the third quarter.

Source: CNBC, TradingEconomics, Yahoo! Finance