Market Recap

US Markets:

Mixed vaccine data weighed on markets on Thursday as the indices closed mixed. After rising for most of the day, U.S. stocks fell in the final hour of trading after reports that Pfizer was scaling back its vaccine rollout plan for 2020 due to supply chain issues. Pfizer now expects to ship only half of the doses it had initially planned to ship in 2020 after finding raw materials in early production that did not meet its standard. However, the report also said that Pfizer and BioNtech are still on track to roll out 1.3 billion vaccines in 2021. The 50 million dose shortfall is expected to be comfortably covered as production ramps up in 2021.

The Dow Jones closed up 86 points, or .29% after gaining more than 200 points at its session high. The S&P 500 pulled back from its two consecutive record closes, and dropped .06% after hitting a new intraday high earlier in the day. The tech-heavy Nasdaq rose 0.23%. Small-caps led the way yet again with the Russell 2000 gaining .60%.

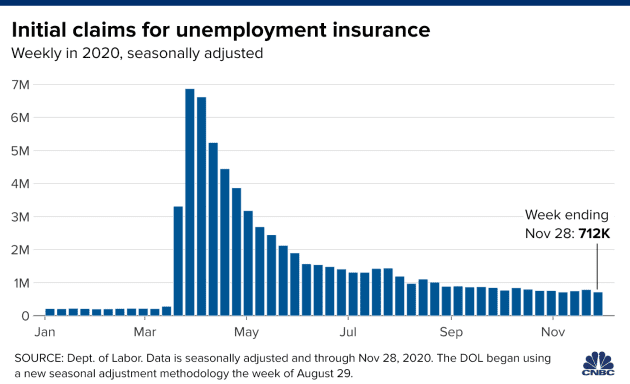

Jobless claims from last week beat expectations, and came in at 712,000. Dow estimates put that figure at 780,000. This is the first time in 3 weeks that jobless claims fell, and was the lowest figure since the pandemic started. Investors are eagerly anticipating the Labor Department’s jobs report for November on Friday. Analysts and economists are expecting that the U.S. economy added 440,000 jobs- a slowdown from the 638,000 in October.

US job cuts also slowed in November, with employers annoucning 64,797 job cuts in November. This figure is below the 80,666 cuts in October, and the second-lowest monthly total for 2020. However, it is 45.4% higher than the 44,569 cuts in the same month last year. The ISM Non-Manufacturing PMI, or indicator for the U.S. services industry, fell to 55.9 in November from 56.6 in the previous month, and was largely in line with forecasts of 56. However, this reading is the slowest increase in the services sector in six months.

House Speaker Nancy Pelosi and Senate Majority Leader Mitch McConnell also spoke on the phone for the first time since the election and discussed a second coronavirus stimulus package. McConnell on Wednesday rejected a $908 billion bipartisan proposal, but said that he sees “hopeful signs” toward reaching an agreement by the end of the year.

In the meantime, COVID continues to rage and accelerate towards record numbers. Over 100,000 patients are currently hospitalized-significantly above any levels hit during the first wave in the spring. 2,800 Covid deaths were also reported- the highest single-day death toll ever reported.

Further stroking the flames of tensions with China, the House of Representatives unanimously passed a bill that would mandate Chinese companies to adhere to U.S. auditing standards if they want to be listed on American exchanges. President Trump is expected to sign the bill into law.

Cryptocurrency:

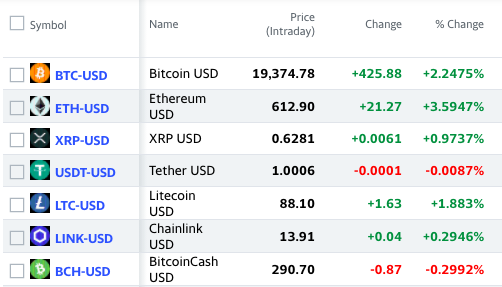

Cryptos ticked upwards today. Bitcoin saw mild gains and broke past the $19,300 level. After hitting an all-time intraday high Monday, and trading as high as $19,864, Bitcoin has somewhat pulled back. Although Bitcoin still has not hit the $20,000 mark yet, it has shattered its previous record high of $19,666 from back in December 2017. Bitcoin’s value is now up over 150% since the beginning of the year, and has been propelled by economic stimulus, validation from public companies such as Paypal, and interest from major investors. Although some believe a Bitcoin correction is inevitable, others believe that it could exceed $20,000 as a hedge against inflation before the end of the year. Ethereum also rose by 3.6% today.

Overall Market:

European equities ended mostly in the red on Thursday, but did not make any drastic moves as investors digested key PMI data, positive coronavirus vaccine news, and Brexit negotiation updates. Frankfurt’s DAX 30 fell 0.4% and the CAC 40 and IBEX 35 were down less than 0.2% while both the FTSE 100 and FTSE MIB saw moderate gains. Markit PMI data confirmed that Europe’s private sector economy contracted in November for the first time in five months amid new lockdowns. However, Pfizer and BioNTech’s vaccine is expected to be available as early as next week after the UK became the first country in the world to authorize it on Wednesday. Other European regulators are expected to rule on the vaccines very shortly. Ireland’s Foreign Minister Simon Coveney also said that there was a good chance that Britain and the EU could reach a post-Brexit trade agreement within the next few days. Canadian stocks continued their surge and rose for the third day in a row on Thursday, closing above the 17,400 level for the first since February.

Oil prices rose more than 1% on Thursday and traded as high as $45.83 a barrel after OPEC+ agreed to a small oil production hike from January by 500,000 bpd.

WHATS UP

Shares of Ralph Lauren Corp (+8.705%), Norwegian Cruise Line Holdings (+8.633%), and American Airlines Group (+8.277%) led the S&P 500, while Moderna rose another 9.972%, and Walgreens (+7.48%), and Boeing (+5.964%) led the Dow.

Shares of Pfizer dropped more than 2% following news of the supply chain issues affecting vaccine production and distribution for the rest of 2020.